METHODOLOGY NOTES

²⁰ The TikTok haul observation reflects a hand-coded sample of US TikTok content in which Miniso-purchased products appear, conducted by Asia Aisle in March and April 2026. Product callouts were transcribed manually from video. This is not a formal survey or an automated speech-recognition study. The pattern noted reflects the sampled population only.

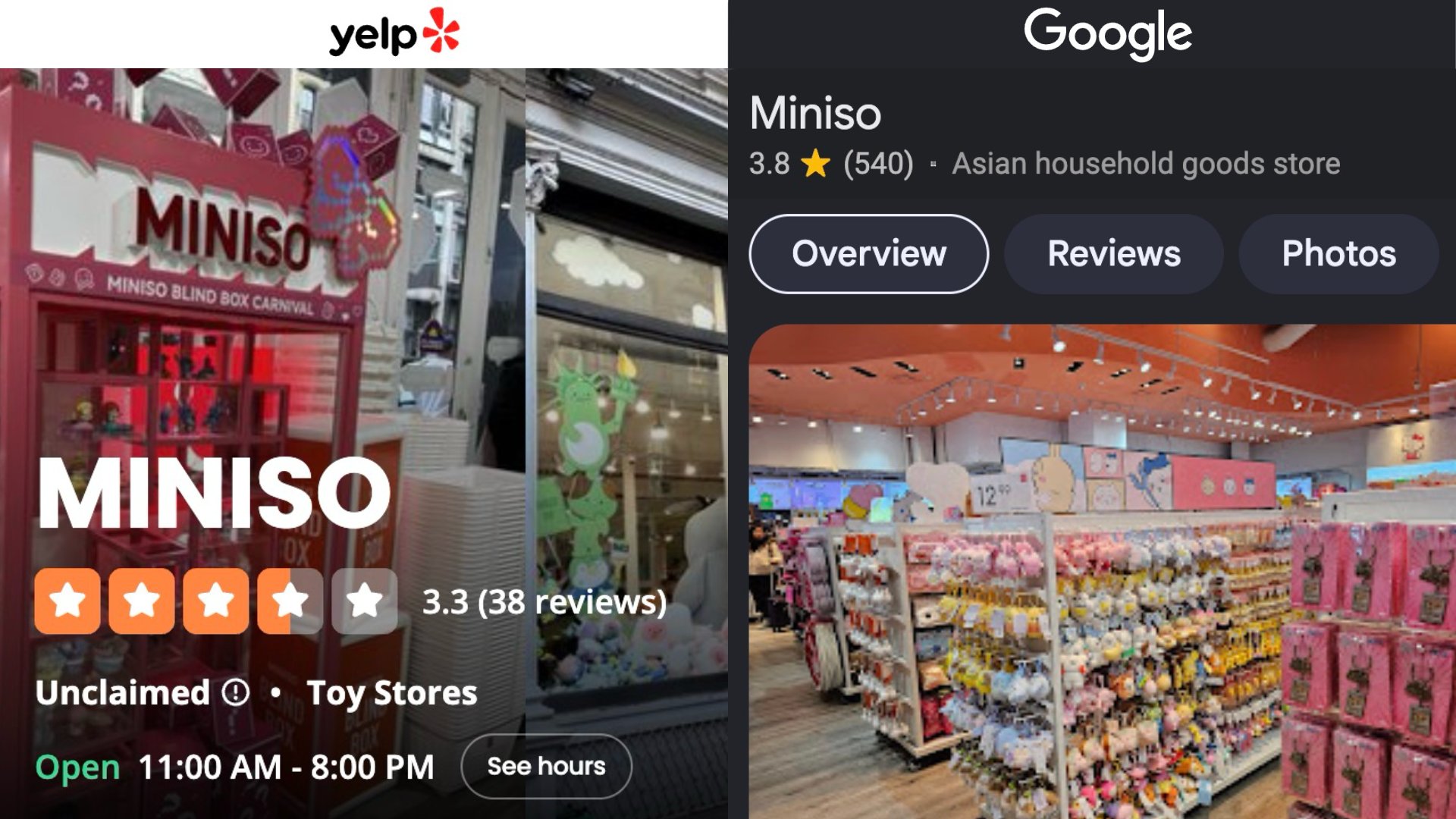

The Yelp and Google Maps category labels for Miniso are observable as of April 2026 and were verified directly. The reader can verify the same labels independently.

The "Major Yo" thought experiment in Section IV is a hypothetical, not a forecast. It is offered to make the contestability of borrowed customer demand visible, not to predict an entrant.

The "What Ye would say" block is the writer's reconstruction of the strongest version of Ye's publicly stated position, drawing on his Group Partner Conference statements (¹⁰) and Miniso's investor disclosures. It is not a direct quotation.

The watch list in the closing section is Asia Aisle analytical inference about which observable moves in the next 24 months would constitute evidence one way or another about whether the second engine is being funded. It is a reading frame, not a forecast.

The Yonghui drag decomposition ($113M Yonghui losses, $39M interest, $22M TOP TOY paper loss) is sourced from Miniso's FY2025 annual results announcement (¹). The categorization of components reflects the company's own disclosure.

The signage-hierarchy renderings in the opening and closing sections are designed editorial illustrations of an observable real-world arrangement at the 5 Times Square Miniso storefront. They are schematic, not photographic. The relative sign sizes reflect the writer's observed dominance of licensor branding over the Miniso wordmark; they are not measured pixel-by-pixel from a single photograph.

Sources

¹ Miniso Group FY2025 Annual Results announcement, March 31, 2026 (NYSE: MNSO; HKEX: 9896).

² Pop Mart 2025 Annual Results, March 25, 2026, filed Hong Kong Stock Exchange (9992.HK).

³ PitchBook Public Comps; companiesmarketcap.com, retrieved May 2026.

⁴ Reuters, "Chinese retailer Miniso to ditch Japanese styling after backlash," August 18, 2022. Vice, "Chinese Discount Retailer Miniso Is Sorry for Pretending to Be Japanese," August 2022. Global Times, August 10, 2022.

⁵ Peter Hays Gries, "China's 'New Thinking' on Japan," The China Quarterly 184, Cambridge University Press, 2005.

⁶ Miniso press release, August 2024. Opening of the 200th US store in Santa Monica.

⁷ Disney Consumer Products Division Launch Conference for Greater China, 2026.

⁸ The Walt Disney Company corporate announcement, March 2021.

⁹ Industry coverage, 2018. Sanrio Inc. wind-down of directly-operated US retail.

¹⁰ Miniso Group Global Partner Conference disclosures, 2024 and 2025.

¹¹ Miniso Group Q4 2025 earnings call transcript, April 2, 2026.

¹² 36Kr, April 2025. Sun Yuanwen, head of TOP TOY.

¹³ Temasek Holdings stake announcement, July 2025.

¹⁴ Miniso Group transaction disclosure, September 23, 2024.

¹⁵ Miniso Group convertible bond offering circular, January 14, 2025.

¹⁶ Pop Mart IPO prospectus (Hong Kong Stock Exchange, December 2020).

¹⁷ Ryohin Keikaku Co. Ltd. annual reports and trade press coverage.

¹⁸ Fast Retailing Co. Ltd. annual reports and trade press coverage.

¹⁹ The Walt Disney Company corporate transaction announcements.

²⁰ Asia Aisle field observation, March to April 2026. See Methodology Notes.

²¹ @TokyoFashion, X (formerly Twitter), August 19, 2022.

²² Yelp brand-page review for Miniso, retrieved April 2026.

²³ Yelp review of Sanrio Surprises, Kahala Mall, Honolulu, HI 96816, retrieved April 2026.